2026 Forecourt Performance Report: Beyond the pump

Canada’s retail petroleum landscape has entered a lean, mature era of network optimization where success is no longer dictated solely by what is sold at the pump.

The 2025 National Retail Petroleum Site Census, published by downstream consulting specialist Kalibrate Canada, Inc. reveals that while fuel retail remains an essential part of Canadian life, the traditional gas station model is undergoing an irreversible structural and operational shift.

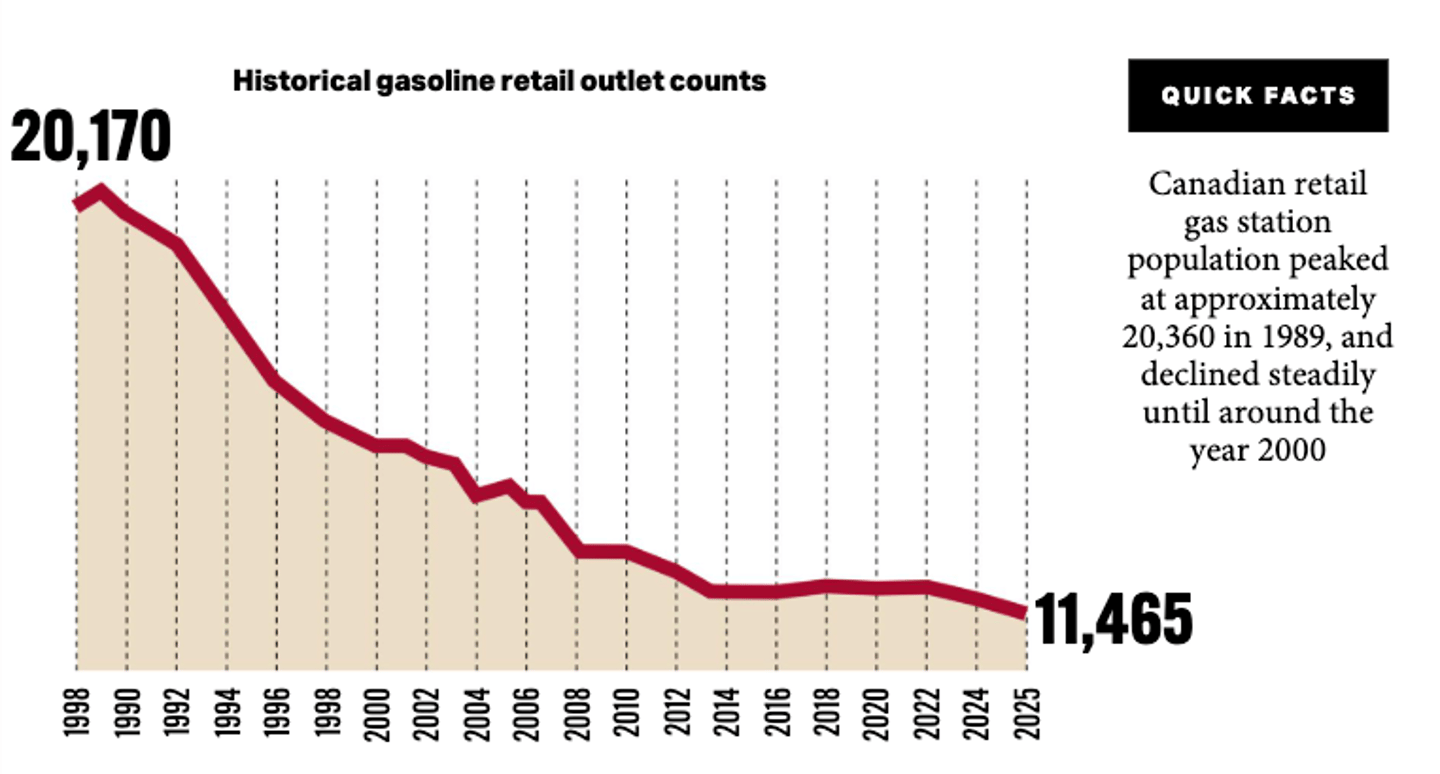

As of Dec. 31, 2025, Canada’s total retail gasoline station count dropped to 11,465 locations, a decline of 146 sites from the prior year and the lowest national site count since tracking began in the late 1980s. Yet Kalibrate notes this isn't a sign of an industry in crisis, but instead “the long-term picture is one of relative stability compared with the steep rationalization that took place in earlier decades: after a dramatic contraction from historical peak levels, the national outlet count has hovered near today’s range for more than a decade, suggesting that the industry has moved into a more mature, slower-changing phase of network optimization.”

For those in the convenience and forecourt business, the report delivers a clear mandate: adapt backcourt offerings, expand loyalty ecosystems and prepare for a highly collaborative retail environment, or risk obsolescence in a shrinking network.

The illusion of big oil control

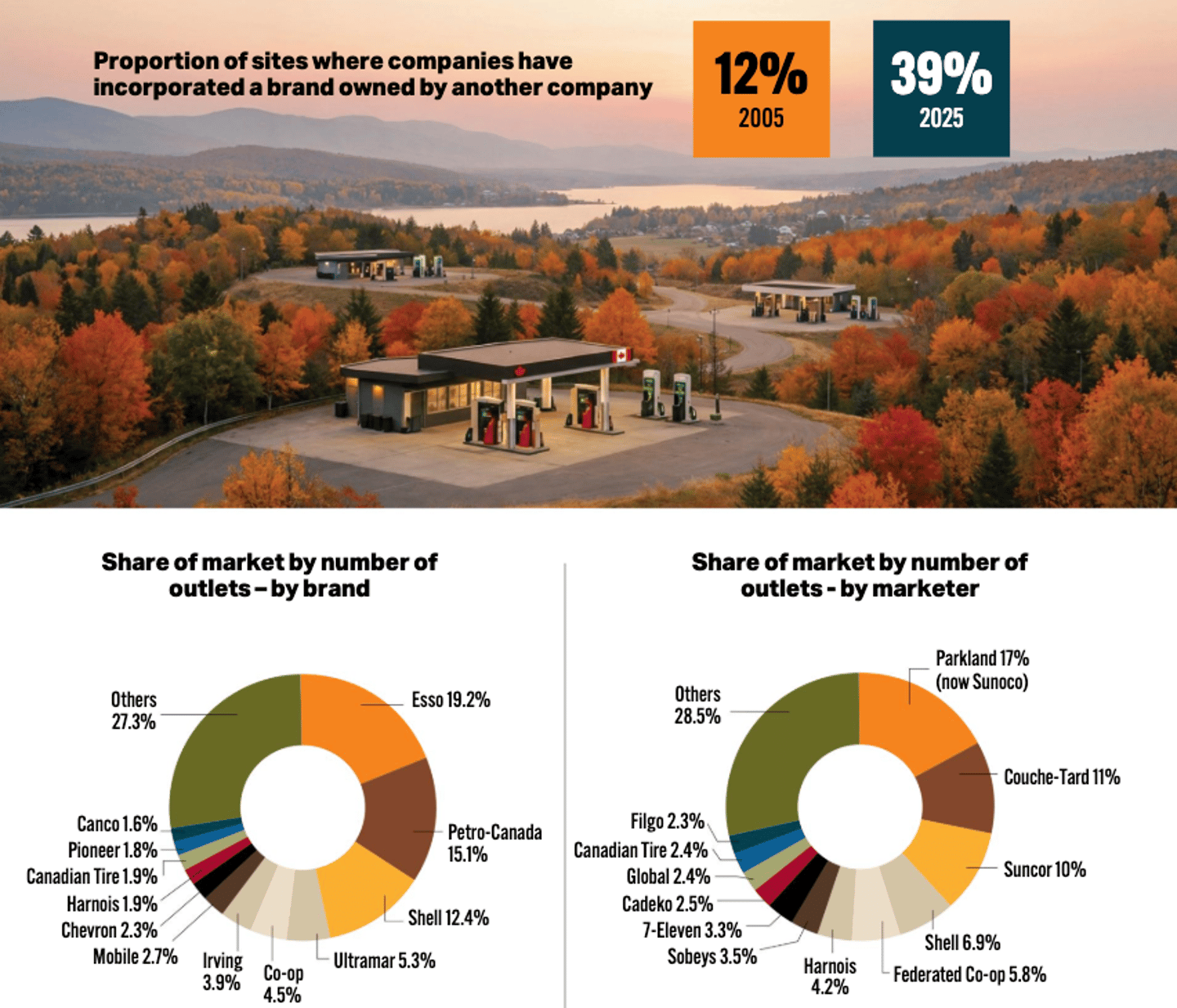

To consumers, Canada’s forecourts appear dominated by corporate oil giants. The top three fuel brands; K, Petro-Canada and Shell, command 47% of all stations across the country. However, the report exposes a major disconnect between the logo on the canopy and who holds the keys to the business.

Only 22% of Canadian gas stations (2,565 sites) are price-controlled by an integrated refiner-marketer. The remaining 78% of pump prices are set by independent proprietary networks, dealers or non-refining marketers.

“The visible brand on the canopy often masks a more nuanced commercial relationship,” Kalibrate states in the report, pointing to an asset-light, partnership-driven retail model that has taken hold of the industry.

Major refiners have steadily shifted operational responsibility and pricing control to a distributed network of regional distributors and independent retail chains.

In 2025, 27 fuel marketing companies incorporated another company's brand into their networks, a strategic arrangement that now accounts for 39% of all stations nationwide.

This allows major refiners to maintain brand equity and secure wholesale fuel supply agreements while leaving local site operations, real estate management and backcourt innovations to specialized retailers who can pivot quickly to changing local demographics.

The backcourt pivot

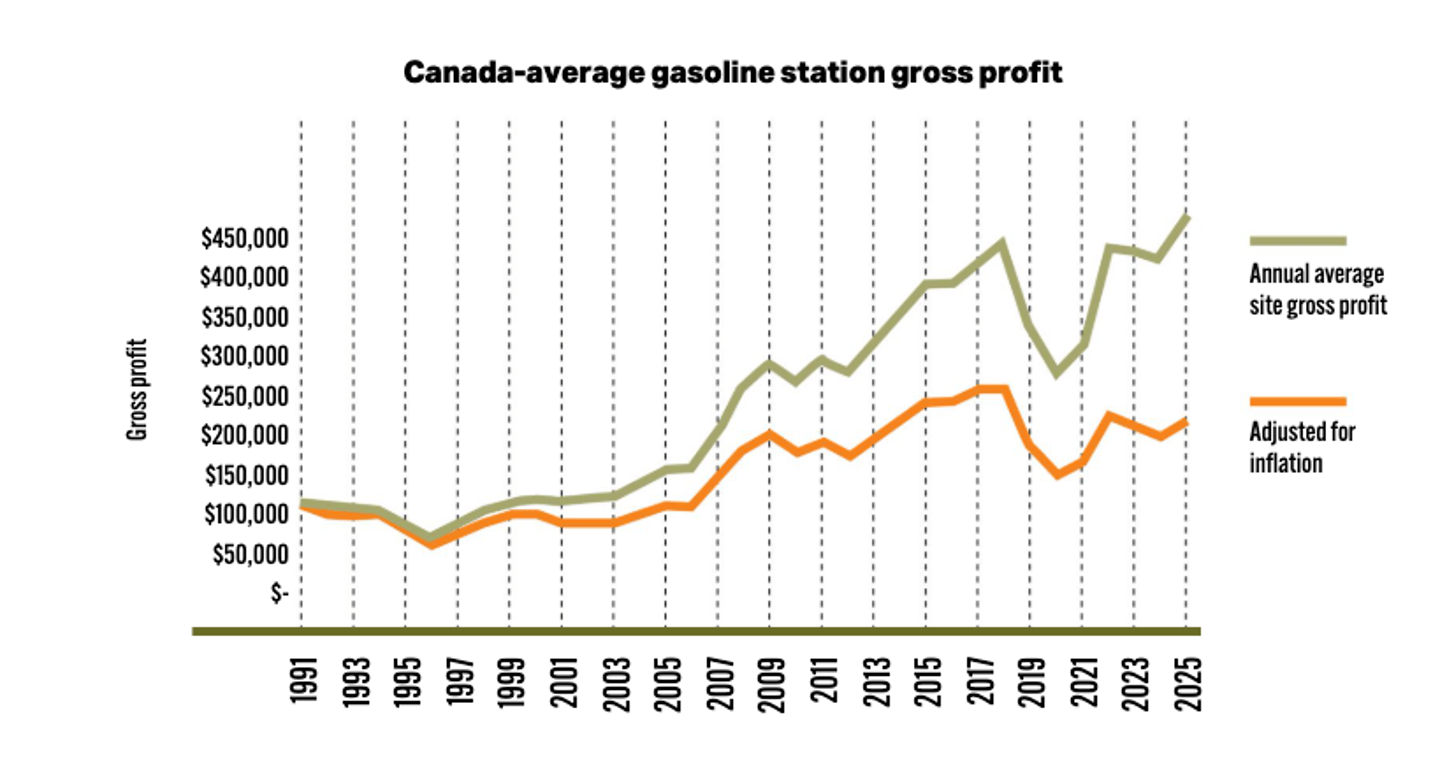

The driving force behind this structural shift is simple economics: fuel retailing is a high-volume, low-margin game. Kalibrate data shows that the national average retail margin component of a 146.5 cents-per-litre pump price was just 10.4 cents in 2025. When adjusted for inflation, actual retail margins have steadily shrunk over the last three decades, dropping from 7.0 cents per litre in 1991 to 5.3 cents per litre today.

While average station gross profits from fuel sales hit an all-time high in 2025 due to recovering fuel volumes, rising operating costs and inflation mean fuel alone cannot support a modern forecourt business. “Non-petroleum offerings are now central to outlet viability and competitiveness,” the report underlines.

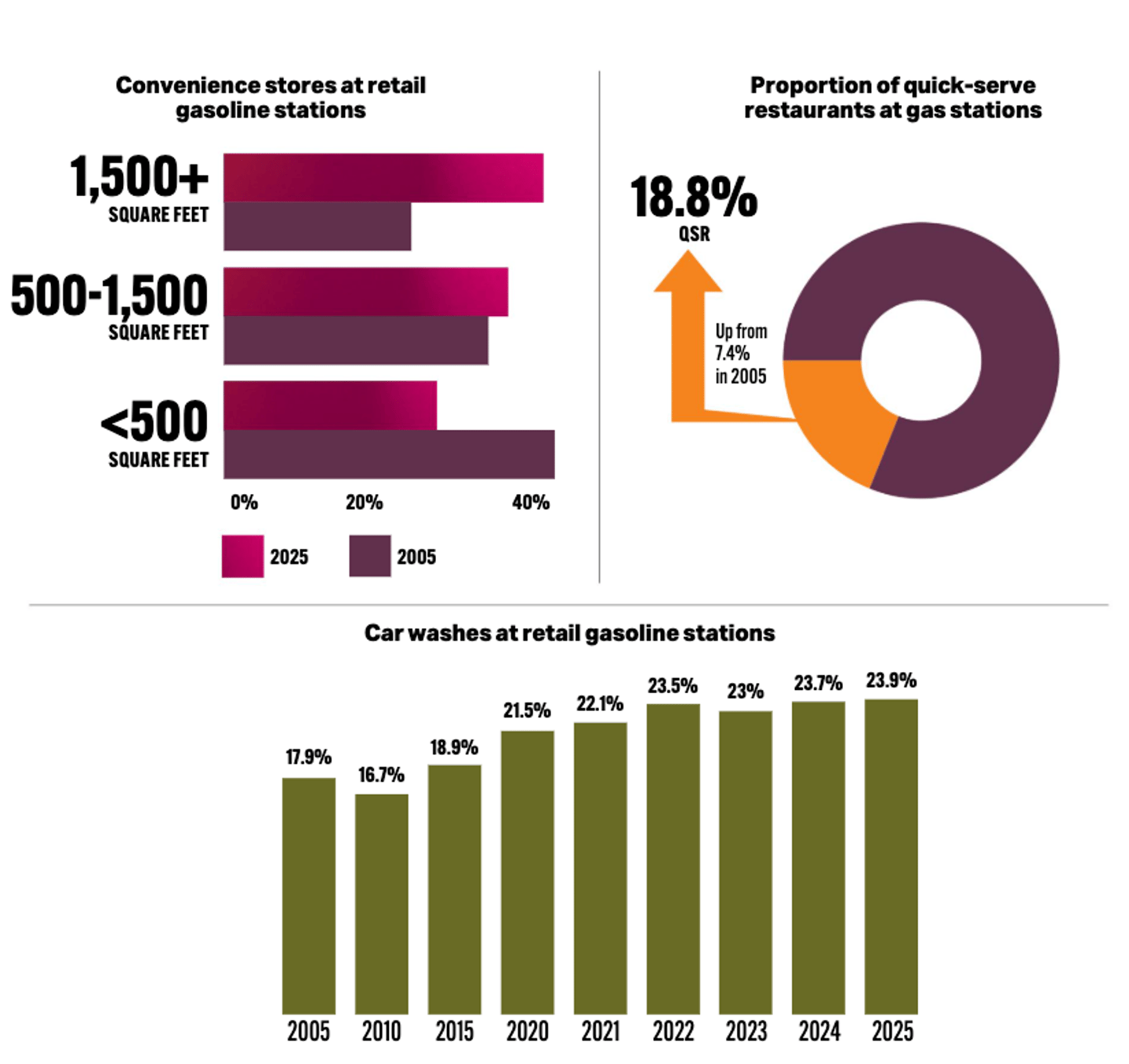

Nearly every gasoline station in Canada features a convenience store of some kind. These c-stores have evolved from the simple payment kiosks of yesterday, into sophisticated retail destinations with expanded services designed to turn the gas station into a convenient community hub. One need only look to store size for evidence: In 2005, small kiosks under 500 sq. ft. made up nearly 42% of the market. In 2025, large-format convenience stores (exceeding 500 sq. ft.) now represent more than 37% of sites, driven by major investments from convenience retail leaders to bolster revenue from new categories, such as beverage alcohol, and foodservice.

The report shows how profit-generating back-court amenities are scaling up:

- Quick-serve restaurants (QSRs): At nearly one in five stations (18.8%), up from just 7.4% two decades ago.

- Car washes: Steadily rising to hit a 23.9% representation rate nationwide.

Non-traditional players reshape competition

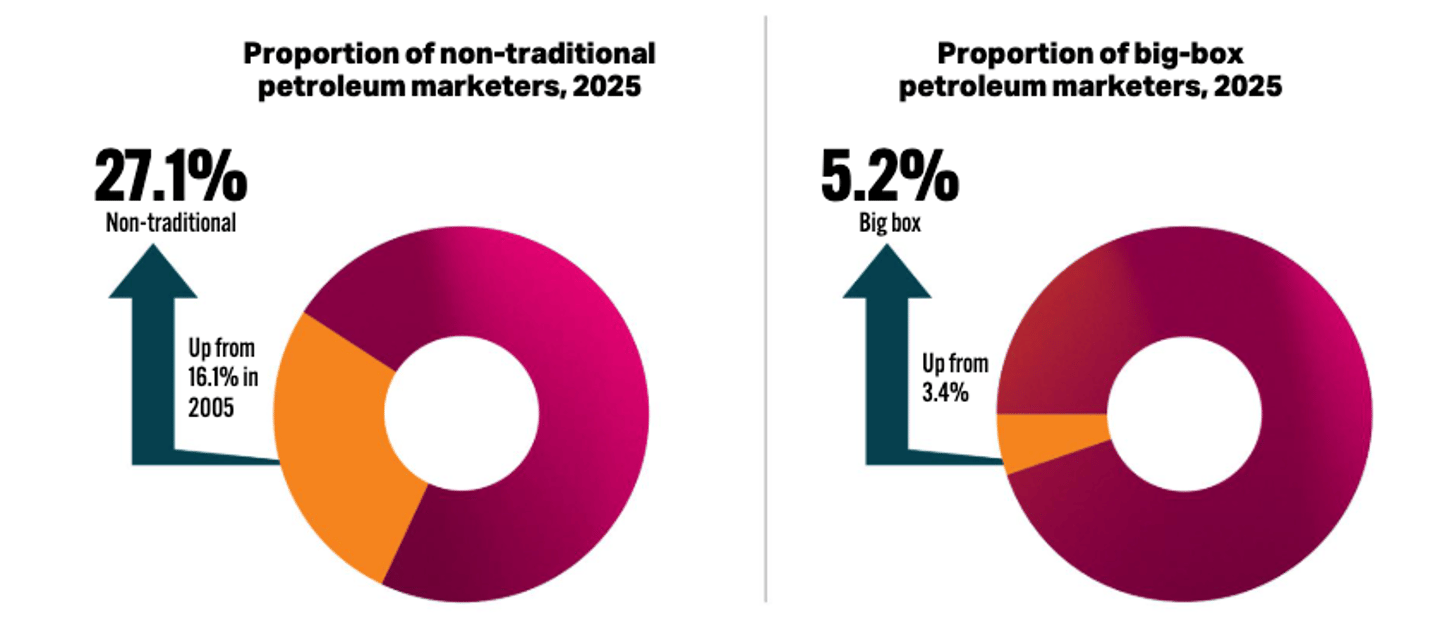

Forecourt professionals are adapting the business model in the face of intense competition from non-traditional marketers—operators whose primary business is grocery, big box or large-format retail rather than petroleum. These networks account for 3,106 outlets, representing 27.1% of all Canadian fuel sites.

The geographic distribution of these players varies. In Western Canada, non-traditional penetration has stabilized or shrunk over the past 20 years. However, Central and Eastern Canada have witnessed an explosion. In Atlantic Canada, non-traditional operators account for 42.4% of the total market, while in Nova Scotia and Prince Edward Island, they make up more than half of all retail outlets.

High-volume retailers (HVRs), such as Costco, use fuel as a loss-leader or cross-promotional tool to drive traffic to their main retail footprint. Because HVRs generate massive fuel throughputs, they maintain a significant pricing advantage due to low operating costs per litre, heavily disrupting local price competitiveness.

Interestingly, the report notes that big box market share has dipped slightly from its historical peaks due to grocery chains selling off fuel assets to focus on core operations. For example, Sobeys Capital divested its Safeway fuel bars to Shell Canada in 2023. However, this year, Shell announced it is replacing its Air Miles program with Scene+ points nationwide. Because Sobeys-owned stores also utilize Scene+, cross-promotions between the grocery giant and adjacent gas stations are back.

Leveraging loyalty ecosystems

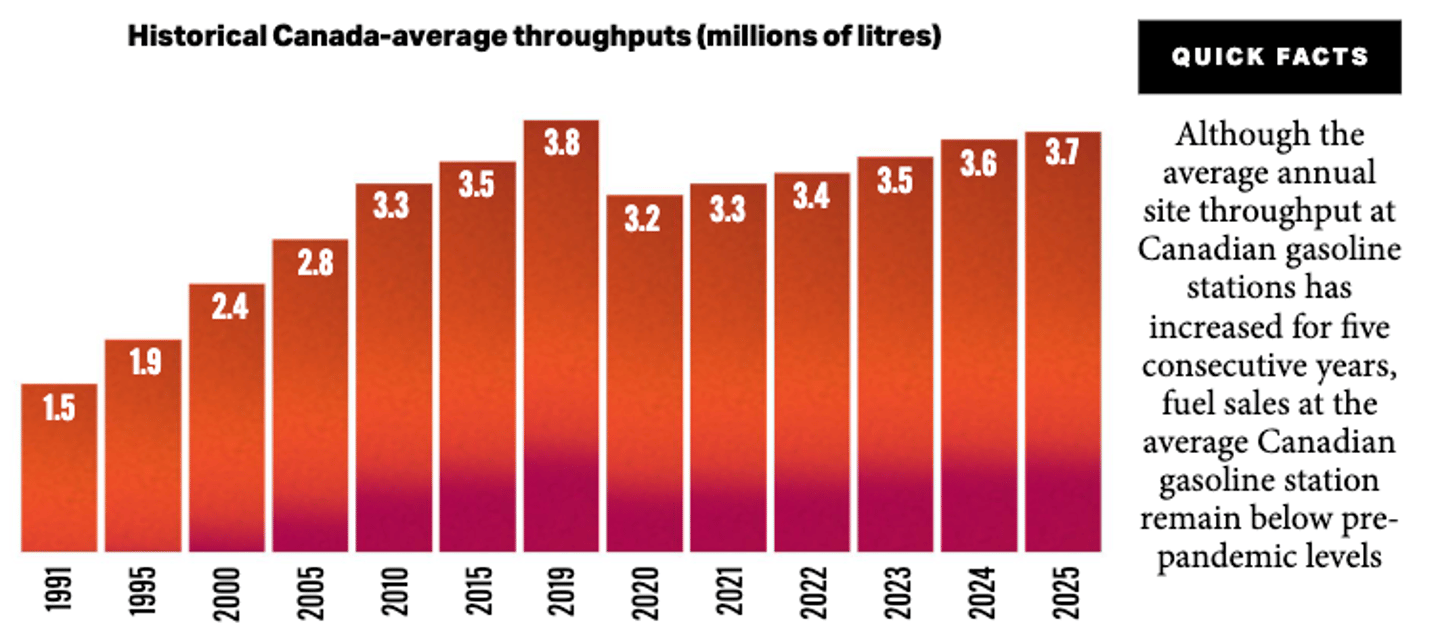

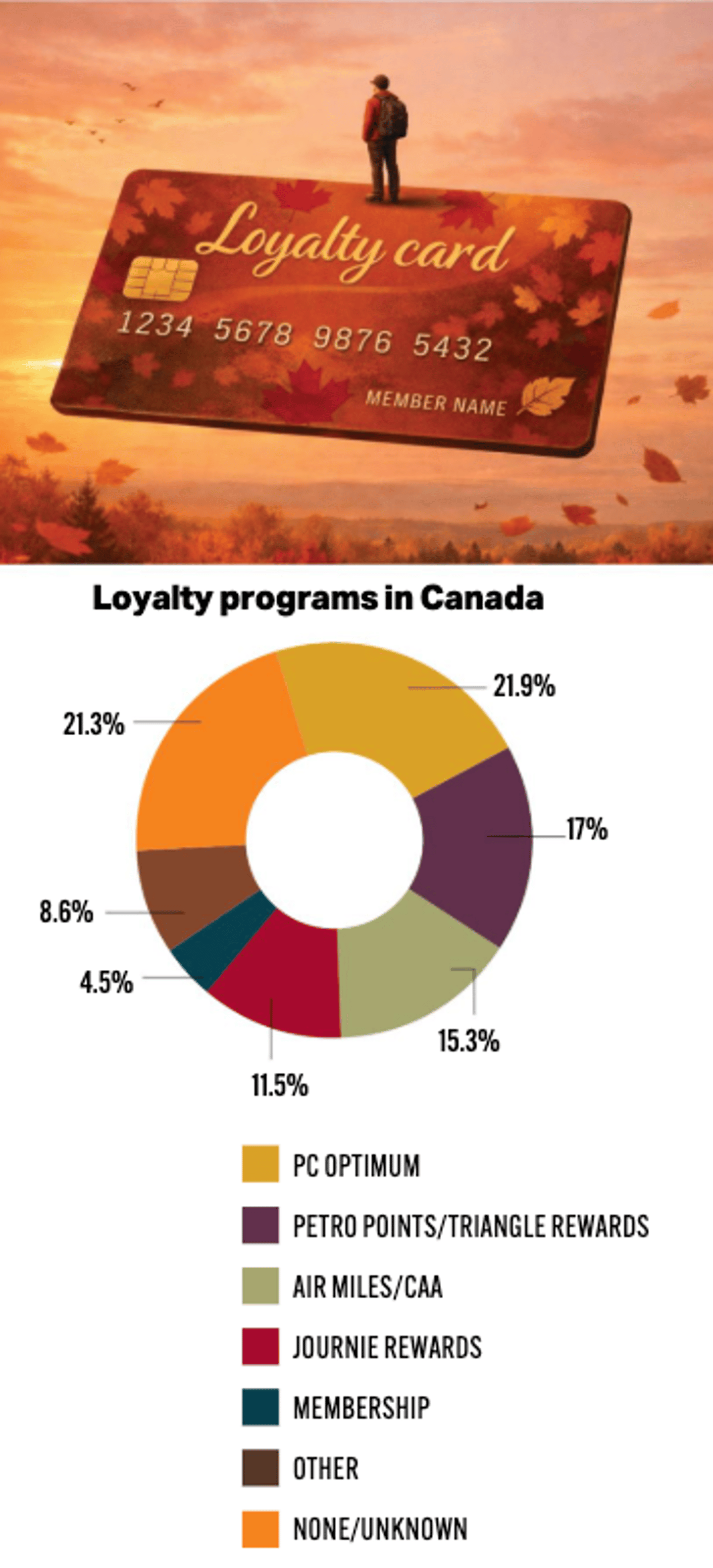

With fuel volumes per station creeping up to 3.72 million litres annually, but still below pre-pandemic levels, capturing consumer “share of wallet” is now hyper-focused on loyalty programs. In 2025, 79% of Canadian gas stations featured a loyalty program, up from 73% in 2023. Four programs—PC Optimum, Petro-Points/Triangle Rewards, Air Miles/CAA discounts and Journie Rewards—account for 66% of the entire loyalty network.

As competition heats up, the report notes: “Loyalty rewards are becoming increasingly complex, with more options for consumers to share loyalty points with non-fuel programs or combine them to increase discounts with various financial institutions.”

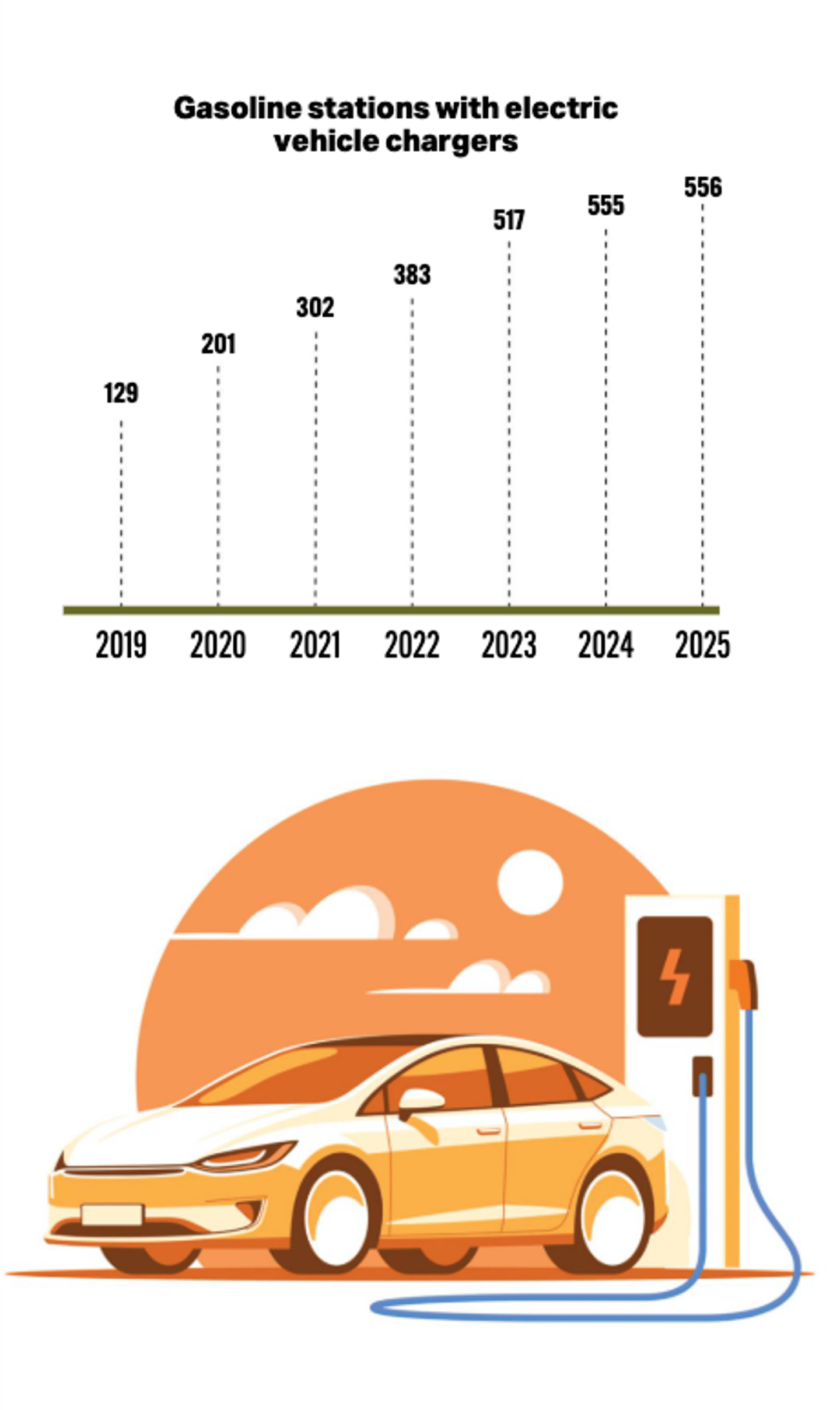

The hybrid forecourt

Zero-emission vehicle (ZEV) adoption has grown to 9.5% of new vehicle sales, however total EV sales dipped last year due to economic uncertainty and shifting incentive programs. In turn, for every single zero-emission vehicle registered in 2025, nearly eight traditional vehicles were sold.

In other words, demand for traditional gasoline and diesel is far from vanishing. As the report concludes, "Even with greater market penetration of electric vehicles, the need for Canadian gas stations will remain strong for many years."

Savvy operators are treating EV infrastructure not as a replacement for fuel, but as a strategic asset. Integrating charging into the traditional forecourt creates a more diversified, resilient business model.

The real value lies in capturing “dwell time.” Unlike the traditional fuel dispenser designed for a rapid three-minute turnaround, EV charging brings in drivers for an extended 20-to-30-minute stay. For the c-store, this behaviour shift is a major catalyst—drawing motivated buyers away from the pumps and into the backcourt, where high-margin convenience, fresh foodservice and premium coffee concepts can thrive.

The bottom line

The future of the Canadian forecourt is a synergistic evolution where success is no longer dictated solely by what is sold at the pump. Data from Kalibrate’s National Retail Petroleum Site Census indicates that the secret sauce is network optimization that seamlessly serves the hybrid driver, while creating a welcoming, amenity-rich retail hub that meets the needs of an evolving convenience-focused customer.

OCTANE is pleased to partner with Kalibrate to share a preview and highlights from the just-released 2025 National Retail Petroleum Site Census. The report, which includes 43 pages of data and deep insights, can be purchased in its entirety via the Kalibrate website. For more information, please reach out to Suzanne Gray, sales and services consultant, at [email protected]